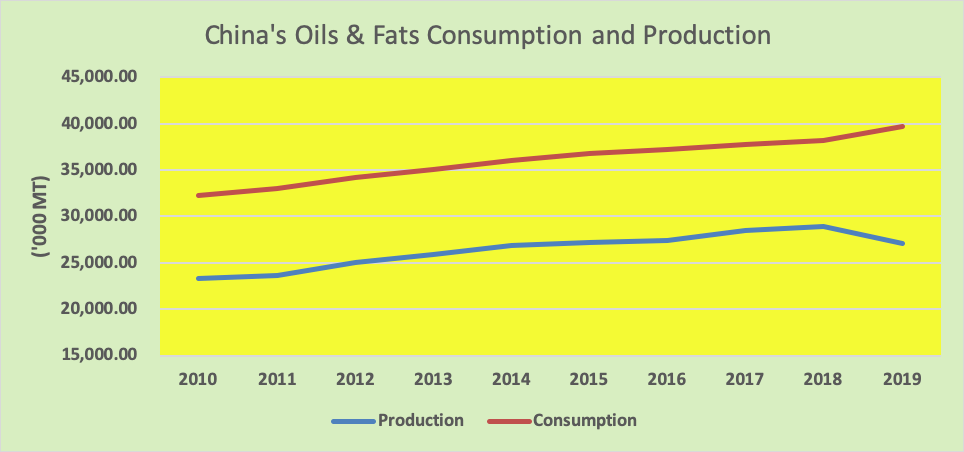

Edible oil consumption in China has been increasing consistently in the last decade due to the accelerating urbanization and improved living condition. Oils and fats consumption also grew from 32.2 million MT in 2010 to 39.7 million MT in 2019. Per capita consumption of oils and fats rose from 23.2 kg to 27.4 kg for the same period in consideration. While edible oil consumption has been growing consistently, local oils and fats production has remained stagnant. This has led China to rely more on imported edible oils to meet its shortfall. From 2011 to 2019, China’s oils and fats import grew by an average annual rate of 5% or 387,200 MT per year. With China’s enormous potential to grow economically, there are opportunities for Malaysian palm oil to capitalize on the rising edible oil demand and increased Malaysian palm oil export. Opportunities for higher palm oil sales also exist in Inner China as growth moves inland with the country’s urbanization programme. There are also opportunities created by the improvement in lifestyle where consumers are shifting their preference towards more healthy food.

Changes in Consumer Preference

A big trend influencing Chinese consumer behaviour is the growing awareness of healthy foods, which has an impact on their purchasing behaviour. Nowadays consumers are more discerning in their choice of oils and fats consumed, and more consumers are shifting from animal fats to vegetable oils due to health concerns. Due to this trend the market share from animal fats is now being substituted by vegetable oil. Based on Oilworld figures, the national average of animal fats to other oils and fats consumption is 12.7% in 2019 and this ratio has been falling at an average rate of 1.7% per year from 2010 to 2019. This development can be capitalized by palm oil players to increase palm oil sales in the country as palm oil is a healthy oil.

Change in consumption pattern is also observed in the rural areas. The rural edible oil consumption is still based on the second grade (degummed and neutralised) oil. With rising income, rural area edible oil consumption is moving towards more healthy refined oil. The National Bureau of Statistics reported that from 2010 to 2018, China’s rural per capita income grew by 12.3% per year to reach 14,617 yuan in 2018. Statista estimated that the region’s per capita income will grew further to approximately 16,000 yuan in 2019. This development provides opportunities for more palm oil to be sold to this region for blending with other soft oils.

The Urbanisation of Rural Area

Following China’s continuous reform policy, the growth of inner China townships has been robust in recent years. The development of the inner China area generated an emerging and new growth market for palm oil products in rural areas. Based on the China National Bureau of Statistics figures, the rural population stood at 551.6 million in 2019. Hence, for every 1 kg increase in oils and fats usage per capita, there will an increase of oils and fats usage by 551,620 MT. Demographically, urban dwellers consume higher oils and fats. In urban areas, per capita consumption is about 23-27kg/person/year, whilst in rural areas, it is about 15-18kg/person/year (Chinaoils.cn). Hence, there is a potential of additional 2.76-6.61 million MT oils & fats to be added into China’s market should per capita consumption among the rural dweller reaches those staying in urban area. While these could be achieved due to the development in rural area, migration of its citizens from rural to urban area is also likely to generate higher growth for edible oil demand in urban area. The migration from rural to urban cities will improve the lifestyle and buying power per capita of the rural Chinese. This will encourage the usage of more refine oils and hence will create more opportunities for palm oil import as it increases opportunities for palm oil to be promoted for blending with other soft oils. The advantage of using palm based blended cooking oil is that palm oil is competitively price and it is a good frying medium.

In China, about 70% of total palm oil is consumed in the food sector, including cooking oil, instant noodles, bakery, confectionery, chocolate, ice-cream sectors, etc. Palm products other than palm oil, also have a good share in non-food sectors, such as oleochemicals sectors, etc.

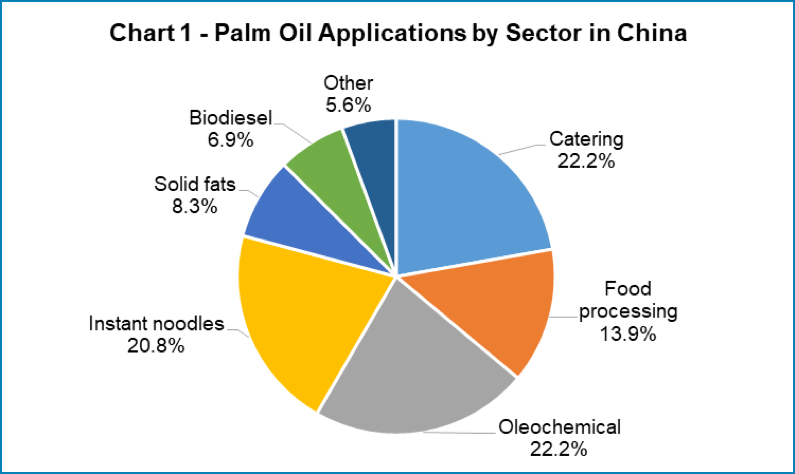

From the breakdown of palm oil application chart in China, it can be deduced that growth in urban usage favours the growth of palm olein usage. This is because RBD palm olein caters for the 2 big sectors that use this palm fraction namely the catering and food processing sector. (Refer to chart 1). There is room for more RBD Palm olein usage in these sectors as the high price spread against soybean oil will give room for more blending of this fraction, on top of the growth of the sector/industry itself. Nevertheless, another major palm product which is widely used in these sectors is frying shortening, but this will not benefit Malaysia’s palm oil industry much as most of China’s shortenings are imported from Indonesia due to competitive price. Malaysia only exported 7,725 MT of shortenings to China in 2019.

Although frying instant noodles also involves using RBD Palm olein or RBD palm oil, the potential of growing palm oil demand from this sector is rather limited as most manufacturers are currently using palm and growth of instant noodles demand in China is rather limited. This is due to the earlier mentioned reason where there is increase preference of healthier products among Chinese consumers and also increase in the disposable income.

However, Malaysia could benefit from higher China’s usage of oleochemical through the exports of oleochemicals and also RBD stearin to support China’s oleochemical production.

Market Development

China’s economic development has created opportunities for sales of more palm oil products. Rising income from continuous economy growth fuels higher purchases of all palm products. In China, the palm oil markets can be grouped into 2 homogeneous regions namely the less developed market in inner regions and the more developed markets located in the coastal region.

For the potential stakeholders’ in rural regions, the awareness of the advantage of palm oil is also low. To assist the industry to grow market share of palm oil to this region, MPOC has been organizing a special programme called TEMPO. This programme focuses on imparting palm oil knowledge and application to the potential buyers from this region.

For the more developed region, the main selling product is RBD palm olein. Oleochemical market sales rank second. The oleochemical sector provides an outlet for high volume sales of raw materials to support China’s oleochemical producers and oleochemical derivatives such as fatty acid and fatty alcohol. There are also opportunities to sell shortenings to the instant noodles producers and specialty fats to the confectionery players. The volume demanded will be much smaller than the RBD palm olein and the oleochemical market.

In conclusion, inner China market has potential to generate high volume sales in future due to its sheer population size and continuous development. Volume of purchase is low currently and confine to packed products. However, this expansion is limited by the hefty transportation cost to transport goods from coastal to inland. In the bulk market which is mostly confined in the coastal area, palm oil products will also grow along with the economy. Main products to market in this region is RBD palm olein and oleochemical. The region also offers prospect for other palm derivatives such as confectionery fats which is traded at much lower volume.

Prepared By: Lim Teck Chaii with Theventharan Batumalai and Desmond Ng

*Disclaimer: This document has been prepared based on information from sources believed to be reliable but we do not make any representations as to its accuracy. This document is for information only and opinion expressed may be subject to change without notice and we will not accept any responsibility and shall not be held responsible for any loss or damage arising from or in respect of any use or misuse or reliance on the contents. We reserve our right to delete or edit any information on this site at any time at our absolute discretion without giving any prior notice.